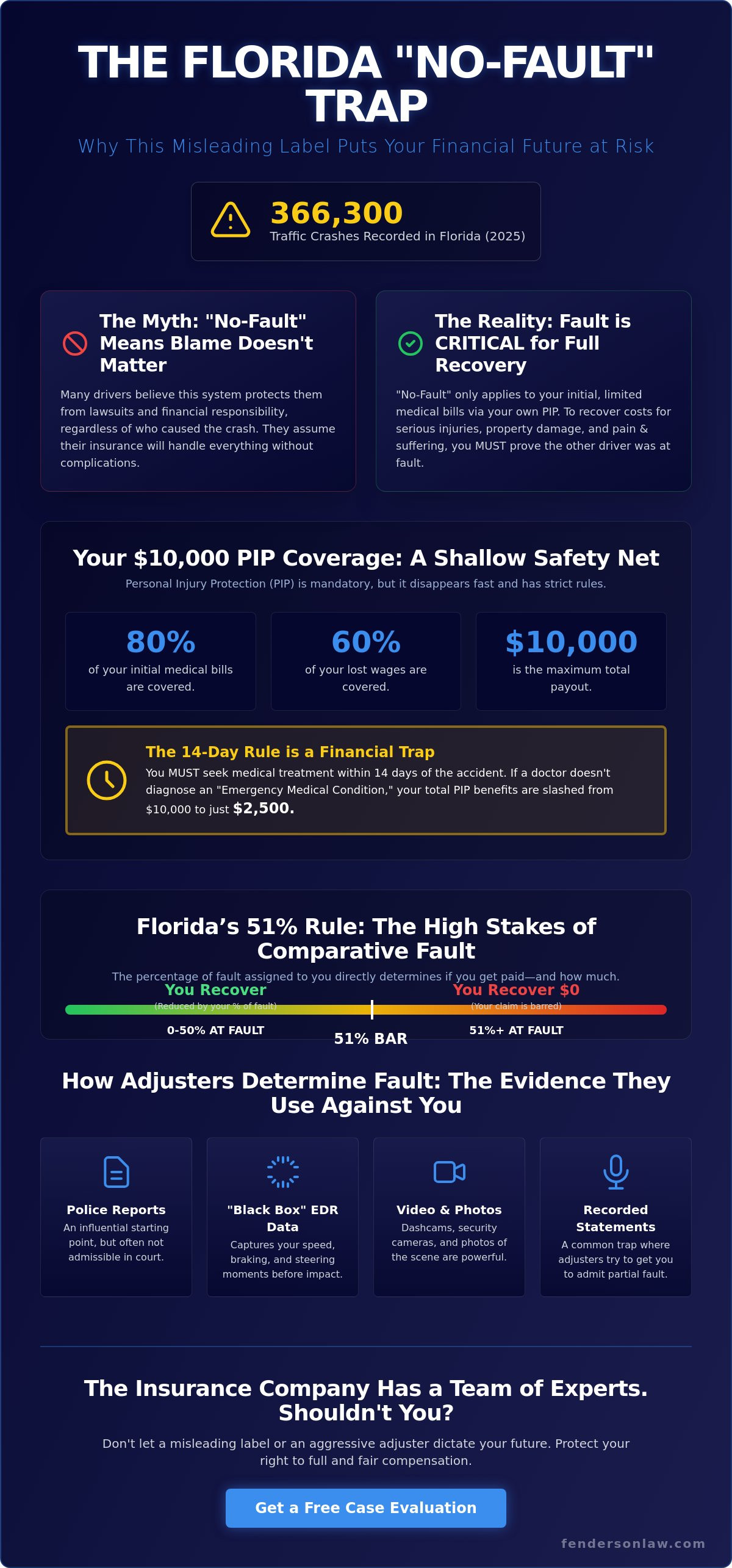

What if the "no-fault" label on your Florida insurance policy is actually a trap designed to lower your guard? Many drivers believe that being at fault doesn't matter in the Sunshine State, but with 366,300 traffic crashes recorded in 2025 alone, that misunderstanding is costing victims their financial security. You’ve likely felt the pressure from aggressive adjusters or the crushing weight of medical bills that quickly exhaust your $10,000 PIP limit. It’s an exhausting, high-stakes struggle where the rules often seem stacked against your recovery.

We understand the fear of being sued personally and the uncertainty of who will actually pay for your car repairs. This article will expose the truth about how liability really works in Florida and why the no-fault system is often just a starting point for complex litigation. You'll discover how to navigate the 14-day rule for medical treatment and protect your settlement from the 51% modified comparative negligence standard. We'll show you how to cross the serious injury threshold and secure the justice you deserve before the two-year statute of limitations runs out.

Key Takeaways

- Grasp why Florida’s "no-fault" status is a misleading label that does not protect you from personal liability or aggressive lawsuits.

- Understand how the strict 51% bar can completely strip away your right to compensation if you are found mostly at fault for the crash.

- Learn to challenge the data from "black boxes" and crash reports that insurance adjusters use to unfairly shift blame and protect their profits.

- Identify the serious injury threshold that allows you to demand full justice and financial recovery beyond the limited reach of PIP coverage.

- Separate fact from fiction regarding rear-end collisions and partial negligence to secure the settlement you need for your future.

The Florida No-Fault Trap: Why the Name is Highly Misleading

Don't let the name fool you. Florida’s "no-fault" designation is one of the most dangerous misnomers in our legal system. It suggests a world where blame doesn't matter and everyone is automatically protected. In reality, it's a rigid insurance requirement that often leaves victims holding the bag for massive expenses. The law forces you to turn to your own insurance first, but that coverage is a shallow safety net that can break under the weight of a real crisis.

Under the No-fault insurance system, every registered vehicle owner in Florida must carry a minimum of $10,000 in Personal Injury Protection (PIP). This coverage is designed to pay for 80% of your medical bills and 60% of your lost wages, no matter who caused the wreck. But here is the catch: $10,000 vanishes in hours at a modern emergency room. If a qualified medical provider doesn't determine you have an "Emergency Medical Condition" within 14 days, your benefits are capped at a measly $2,500. Once those meager funds are exhausted, you are left vulnerable unless you can prove the other driver was at fault.

When Does 'No-Fault' End and 'At-Fault' Begin?

Insurance adjusters want to keep your claim trapped inside the "no-fault" box. Why? Because it limits their financial exposure and protects their profits. To break out of this system and seek full compensation for pain and suffering, your injuries must meet the "serious injury threshold." This isn't a suggestion; it's a legal barrier you must overcome. You must demonstrate a permanent loss of a bodily function, significant and permanent scarring, or a permanent injury within a reasonable degree of medical probability. If your life has been fundamentally altered, the no-fault rules no longer apply. You have the right to pursue the responsible party for the full scope of your damages.

Property Damage: The Immediate At-Fault Reality

Many drivers are shocked to learn that PIP doesn't cover a single cent of vehicle repairs. If your car is totaled or your motorcycle is wrecked, your "no-fault" policy won't fix it. This is where being at fault becomes an immediate, high-stakes reality. Florida requires drivers to carry $10,000 in Property Damage Liability (PDL). This coverage kicks in from the very first dollar to pay for the damage the liable driver caused to your property. Determining responsibility isn't just a legal formality; it's the vital first step in getting your vehicle back on the road and your life back on track.

How Florida Adjusters Determine Who is Truly At Fault

Who decides your fate after a crash? You might think the police officer has the final word, but insurance adjusters are the ones pulling the strings behind the scenes. They don't work for you. They work for a corporation’s bottom line. Their goal is simple: find any reason to name you at fault so they can slash your payout. They sift through the Florida Traffic Crash Report, but they also dig deeper into digital footprints you might not even know exist.

Modern cars are snitches. Most vehicles now carry an Event Data Recorder (EDR), often called a "black box." This device captures your speed, braking patterns, and steering angles in the seconds before impact. Adjusters also scour the neighborhood for Ring doorbells, dashcam footage, and witness accounts. They are building a case against you from the moment the 911 call is placed. If you've been hurt, having a professional evaluate the legal evidence in your car accident case is the only way to level the playing field.

The Police Report vs. Legal Reality

Did the officer get it wrong? It happens more often than you think. While a police report is a powerful tool for insurance companies, it isn't always the final authority in a courtroom. In Florida, the "accident report privilege" often prevents the report itself from being used as evidence in a civil trial. This gives your legal team the opportunity to conduct an independent investigation. We look at the physical evidence adjusters ignore: the length of skid marks, the timing of traffic signals, and the impact of Florida’s weather on visibility. Under Florida Statutes section 768.81, the specific percentage of blame assigned to each party dictates your recovery. An independent investigation ensures that percentage is fair and accurate.

Adjuster Tactics: The 'Recorded Statement' Trap

Why is the adjuster calling you so quickly? They want a recorded statement before you've had time to process the trauma or speak to a lawyer. They are trained to lead you into a "million-dollar mistake." A simple "I'm sorry" or "I didn't see them until the last second" is interpreted as an admission that you were at fault. You have a legal duty to cooperate with your own insurance company, but you have no obligation to speak with the other driver's adjuster. Their friendly tone is a tactic. They aren't looking for the truth; they are looking for a way to deny your claim. Never give a statement without a protector by your side.

5 Dangerous Myths About Being At Fault in a Florida Crash

Confused by the conflicting advice from friends and insurance agents? You aren't alone. Insurance giants rely on a sea of misinformation to protect their bottom line. They want you to believe myths that make you give up on your claim before you even start. We are here to dismantle these lies and act as the shield your future requires. Let's set the record straight on what it actually means to be at fault in Florida.

- Myth 1: "If I'm partially to blame, I get nothing." This is a massive lie. While laws changed in 2023, you aren't automatically barred from recovery just because you made a mistake.

- Myth 2: "The rear driver is always 100% responsible." While there is a legal starting point for rear-end crashes, it isn't an absolute rule. Sudden stops or mechanical failures change the narrative.

- Myth 3: "PIP is all the coverage I'll ever need." A $10,000 limit is often exhausted before you even leave the hospital. It is a starting point, not a finish line.

- Myth 4: "No ticket means I'm not liable." A police officer's decision not to issue a citation doesn't stop an insurance adjuster from blaming you. Civil liability and traffic tickets are two different worlds.

- Myth 5: "Insurance formulas are fair." Adjusters use software programmed to save the company money. There is no fairness in a corporate algorithm.

Busting the 'Partial Blame' Barrier

Florida currently follows a modified comparative negligence system. This means your financial recovery is reduced by your percentage of blame. If a jury finds you 20% responsible for a crash, you can still recover 80% of your damages. However, the stakes are now higher than ever. If you are found more than 50% at fault, you recover zero. Insurance companies will fight tooth and nail to push your blame over that 51% threshold. You need an aggressive advocate who knows how to push back and fight for a 0% fault rating to maximize your justice.

The Rear-End Collision Misconception

In Florida, there is a rebuttable presumption that the rear driver is negligent. But rebuttable is the key word. This presumption can be defeated. Did the lead driver cut you off? Were their brake lights non-functional? Did they stop abruptly for no reason in a high-speed lane? Fenderson Law Firm investigates the why behind the impact. We don't just look at who hit whom; we analyze the mechanical failures and illegal maneuvers that forced the collision to happen. Our firm stands as a seasoned warrior against the lazy assumptions that insurance companies use to deny valid claims.

Florida’s 51% Rule: The High Stakes of Comparative Fault

The legal landscape in Florida shifted beneath your feet in March 2023. With the passage of House Bill 837, the state moved from a "pure" comparative negligence system to a "modified" one. This isn't just a technicality; it's a financial cliff. Before this change, you could recover damages even if you were 90% responsible for a crash. Today, the rules are far more aggressive. If a jury decides you are 51% or more at fault for your injuries, you are legally barred from recovering a single cent from the other party.

Insurance companies are fully aware of this cliff, and they are eager to push you over the edge. They don't need to prove you caused the entire accident. They only need to find enough negligence to tip the scales to 51%. Every phone call from an adjuster and every question from a defense lawyer is a calculated attempt to shift a few more percentage points of blame onto your shoulders. You need a shield. You need a legal team that understands these high-stakes calculations and refuses to let a billion-dollar corporation rewrite the facts of your crisis.

Calculating Your Recovery Under Modified Comparative Negligence

How much is a single percentage point worth? Imagine you have $100,000 in total damages, including medical bills, lost wages, and pain and suffering. If your attorney proves the other driver was 100% responsible, you receive the full $100,000. However, if the insurance company successfully argues you were 20% at fault for speeding or being distracted, your recovery drops to $80,000. That 20% "minor mistake" just cost you $20,000. If they push that number to 51%, your $80,000 recovery becomes zero. This is why aggressive negotiation isn't just a bonus; it's a necessity for your survival. Fenderson Law Firm acts as a determined protector in the negotiation phase, shaving off every possible point of blame to put more money in your pocket.

Protecting Your Future from Blame-Shifting

Defense attorneys are seasoned in the art of distraction. They will look at the weather, your phone records, and even your choice of footwear to maximize your perceived negligence. We counter their tactics with cold, hard science. Our firm utilizes accident reconstruction experts who can map out the physics of the crash to prove the other driver's primary liability. We don't guess; we prove. You can learn more about our Jacksonville car accident tactics and how we dismantle defense arguments. If you've been injured, don't wait for the insurance company to build a case against you. Secure a dedicated car accident lawyer who will act as your guardian in the metaphorical struggle for justice.

Why 'No-Fault' Doesn't Mean 'No Lawyer': Your Path to Justice

Will you let a billion-dollar insurance corporation dictate the value of your health? The "no-fault" label is a corporate convenience, not a shield for your rights. These companies are for-profit entities that thrive by minimizing your trauma and maximizing their margins. They want you to believe that PIP is your only option. They want you to accept a low-ball settlement before you realize the true extent of your injuries. We refuse to let that happen. Our firm acts as a seasoned warrior for those whose lives have been upended by negligence.

A free consultation is your first line of defense. It allows us to determine if your situation exceeds the no-fault threshold, opening the door to full compensation. If the other driver was at fault, you shouldn't be the one paying the price for their recklessness. We evaluate the evidence, calculate your long-term needs, and build a wall between you and the adjusters who want to see you fail. Our commitment is absolute: we don't get paid unless we win your case. This financial guarantee ensures that every victim has access to formidable representation, regardless of their current financial hardship.

Fenderson Law serves as a beacon of justice across the entire state. Whether you are in Jacksonville, Orlando, Tampa, or Miami, our reach is omnipresent. We understand the specific rhythms of Florida’s roads and the unique tactics used by local adjusters to deny claims. Distance is never a barrier to high-stakes legal representation. We are ready to stand as your long-term guardian in the metaphorical struggle for justice and recovery.

The Fenderson Advantage: Aggressive Advocacy

Navigating Florida’s complex liability laws requires more than just a lawyer; it requires a Determined Protector. We don't just fill out forms. We dismantle the defense’s arguments and secure compensation for medical bills, lost wages, and pain and suffering that PIP simply ignores. The clock is ticking. Florida law now provides only two years from the date of the accident to file a personal injury lawsuit. Evidence like skid marks, vehicle telematics, and surveillance footage can vanish within days. Delay is the enemy of justice. Acting now is the only way to ensure your story is told and your future is protected from those who would see you silenced.

Take Control of Your Recovery Today

The uncertainty following a crash is paralyzing, but you don't have to face it alone. You can take control of your recovery right now by preparing for a professional case evaluation. Gather your medical records, the Florida Traffic Crash Report, and any photos you took at the scene. We will handle the heavy lifting. We take the burden of the legal struggle off your shoulders so you can focus on physical and emotional healing. If you are ready to stop being a victim and start being a victor, the next step is clear. Shield your future—Contact Fenderson Law for a free consultation today.

Take Back Control of Your Financial Future

Florida’s roads are inherently unpredictable, but your legal protection must be absolute. You have seen how the $10,000 PIP limit serves as a shallow safety net and how the 2023 shift to modified comparative negligence can strip you of every cent if you are found at fault. These are not just administrative rules; they are weapons used by massive insurance corporations to protect their bottom line at your expense. You deserve a warrior who understands the high stakes of your personal recovery and refuses to back down.

Since 2010, Fenderson Law has acted as a formidable ally for victims across Jacksonville, Orlando, Tampa, and Miami. We provide the aggressive advocacy required to dismantle blame-shifting tactics and secure the justice your family needs. Our promise is simple and performance-based: we work on a contingency fee basis, meaning you pay nothing unless we win your case. Don't let a for-profit adjuster decide what your future is worth. Shield your future—Schedule your free consultation with Fenderson Law now.

Your path to justice starts with a single, decisive action. You have the power to demand a fair outcome, and we are ready to stand by your side as your long-term guardian until it is achieved. Let's begin your journey toward recovery together today.

Frequently Asked Questions

Is Florida still a no-fault state for car accidents in 2026?

Yes, Florida remains a no-fault state as of May 2026. Recent legislative attempts to repeal the Personal Injury Protection (PIP) system, such as Senate Bill 522 and House Bill 769, did not pass during the 2026 session. This means you are still required to carry $10,000 in PIP coverage to pay for your own initial medical expenses and lost wages, regardless of who caused the collision.

Can I be sued if I am at fault in a car accident in Florida?

Yes, you can be sued personally if the other driver's injuries meet the state's serious injury threshold. While PIP covers minor injuries, it doesn't provide immunity for significant harm. If the accident resulted in permanent injury, significant scarring, or death, the "no-fault" protections vanish. You could be held liable for damages that far exceed your insurance policy limits, putting your personal assets at risk.

What happens if both drivers are found at fault in Florida?

Florida follows a modified comparative negligence system where damages are apportioned by your percentage of blame. If you are found 51% or more at fault, you are legally barred from recovering any compensation from the other driver. If your blame is 50% or less, your total payout is reduced by that specific percentage. This makes every point of assigned negligence a direct hit to your financial recovery.

Does 'no-fault' mean I can't get money for my pain and suffering?

No, you can still recover money for pain and suffering, but you must first step outside the no-fault system. This requires proving that your injuries are permanent or resulted in significant scarring or loss of bodily function. Once you cross this threshold, you can pursue the liable party for non-economic damages that PIP insurance never covers. An aggressive advocate is necessary to prove these "invisible" injuries to an insurance company.

How long do I have to determine who was at fault after a crash?

You have exactly two years from the date of the accident to file a personal injury lawsuit in Florida. While this is the legal deadline, the window to gather evidence like dashcam footage or witness statements is much smaller. Waiting too long allows insurance companies to build a narrative that places the blame on you. Acting quickly is the only way to ensure the facts aren't distorted over time.

What if the other driver was at fault but has no insurance?

If the other driver was at fault but lacks insurance, your own PIP coverage will still pay its portion of your medical bills. To recover damages beyond that limit, you must turn to your own Uninsured Motorist (UM) coverage. If you don't have UM, seeking compensation becomes significantly more difficult. You may have to pursue the driver's personal assets through a civil judgment, which requires a seasoned legal warrior.

Can I change my mind about being at fault after talking to an adjuster?

Changing your story after admitting blame to an adjuster is an uphill battle. Insurance companies use recorded statements as permanent evidence to deny claims or shift liability. While you can clarify or correct facts later with a lawyer's help, your initial admission will be used to undermine your credibility. This is why you should never discuss the details of the crash without a protector by your side.

Why did my insurance company say I'm at fault when I didn't get a ticket?

A police officer’s decision not to issue a ticket doesn't mean you are legally in the clear. Insurance adjusters conduct their own investigations using "black box" data and internal formulas to assign blame. They often use minor technicalities or weather conditions to name you responsible even if no laws were broken. Their goal is to protect their profits, not to mirror the findings of the police report.